On Sunday, December 27, 2020, the President signed into law one of the longest bills in US history. This bill, the Consolidated Appropriations Act 2021, is a sprawling 5,593 pages and contains a $900 billion relief package for aid related to the COIVD19 pandemic as well as a $1.4 trillion in annual funding for the federal government in the upcoming year.

Paycheck Projection Program (PPP)

Clarification of Tax Treatment for Forgiveness of Covered Loans. The Consolidated Appropriations Act of 2021 confirms Congress’s original intent in the CARES Act and reverses the Treasury Department’s interpretation of the tax implications of loan forgiveness, clarifying that PPP loan forgiveness will not be included in the gross income of an eligible recipient nor will any deductions paid for with PPP proceeds be disallowed or have it’s tax attributes reduced.

Covered Period Selection. Borrowers have the option of selecting any covered period length between 8 and 24 weeks after the loan origination date.

Additional Eligible Expenses. Employer-provided group insurance benefits are now considered forgivable payroll costs. The 60/40 ratio (60% payroll expenses and 40% other expenses to achieve 100% forgiveness) has not been changed, but “other expenses” can now include expenses other than rent and utilities. This change only applies to loans that have not been forgiven yet. Additional eligible expenses include:

- Operations expenditures such as software, product delivery, processing fees, or tracking of payroll expenses

- Costs related to property damage and vandalism or looting that occurred during 2020 but were not covered by insurance or other compensation. Supplier costs, including those prior to the covered period that were essential to operations

- Worker protection expenditures (PPE and investments to help recipient comply with federal health and safety guidelines)

PPP Round 2. The Act has provided for a second round of PPP loans. To qualify:

- Revenue must have decreased by 25% (any quarter in 2019 vs. the same quarter of 2020)

- Must have been in operation on February 15, 2020.

- Must have 300 employees or less

- Must not be a publicly traded company

- Must have used all of the first PPP loan in order to apply for second PPP loan

Borrowers may receive a loan amount of up to 2.5x the average monthly payroll costs incurred or paid during 2019 or the one year period prior to the date on which the loan is made, not to exceed $2 million. Entities in industries assigned to NAISC Code 72 (Accomodation and Food Services) may receive loans of up to 3.5x average monthly payroll costs.

Simplified Loan Forgiveness. Loan forgiveness application and documentation is simplified for loans up to $150,000, which will be forgiven in full when the borrower signs and submits certification providing information regarding the number of employees retained, the estimated amount spent on payroll expenses, and the total loan value.

Borrowers who have returned all or part of their PPP loan can reapply for the maximum amount forgivable as long as they have not received forgiveness. They can also work with lenders to modify the loan value if loan calculations have increased due to changes in interim final rules.

Economic Injury Disaster Loan (EIDL)

Extension of EIDL Applications: The Consolidated Appropriations Act of 2021 extended the application deadline for EIDL loans through December 31, 2021. Eligible small businesses can still apply for a maximum loan amount of $2 million, and are now eligible to receive the full $10,000 advance grant regardless of the number of workers employed (previously $1,000 per employee).

EIDL Advance Grant and PPP Loan Forgiveness: The provisions from the previous CARES act reducing PPP loan forgiveness by the amount of advance grant received was repealed with the new act. EIDL Advances will no longer reduce PPP forgiveness.

Tax Implications: The grants remain excluded from income, and no deductions are disallowed as a result of this income exemption.

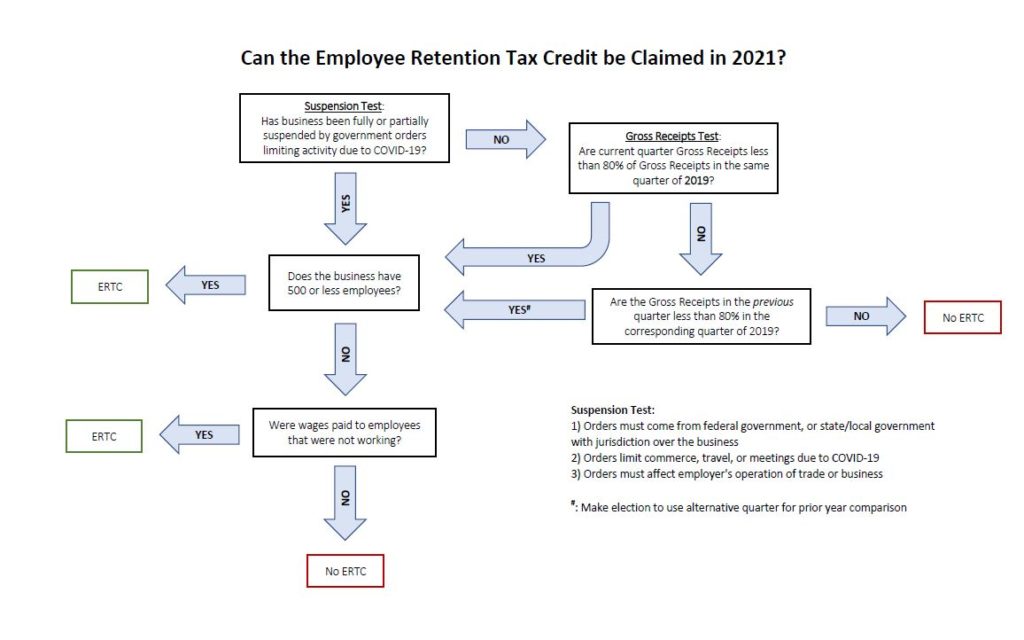

Employee Retention Tax Credit (ERTC)

ERTC and PPP Loans. Employers who have received a PPP loan can now also qualify for the ERTC retroactively. To prevent double dipping, qualified payroll that have been taken into account for PPP loan forgiveness will not be eligible for purposes of determining the ERTC for that period. The ERTC however can be applied to qualified wages paid for using the PPP proceeds that were not forgiven by the SBA..

Tax Credit Hike. Beginning January 1, 2021, the ERTC rate has been increased from 50% to 70% of qualified wages. The $10,000 qualified wage limitation has also been increased to $10,000 per quarter, previously having been limited to the first $10,000 in wages per employee, per year. As a result, employers can now enjoy a maximum credit of $7,000 for each employee per quarter, as opposed to the previous $5,000 max credit per employee for wages paid after March 12, 2020 and before January 1, 2021. .

Eligible Employers Modifications. The Act expanded the gross receipts test for eligible employers, reducing the required gross receipt decline from 50% to 20% of the comparable quarter. The comparable quarters are determined as follows:

- For businesses that started operations in 2019 – same calendar quarter in 2019 and 2020 (i.e. 2019 Q3 vs 2020 Q3)

- For businesses that started operations in 2020 – same calendar quarter in 2020 and 2021 (i.e. 2020 Q1 vs 2021 Q1)

- Alternative Election – businesses can elect to compare immediately preceding quarters (i.e. 2020 Q1 vs 2019 Q4)

- The above modifications are available to employers beginning January 1, 2021.

The above modifications are available to employers beginning January 1, 2021.

Extended Availability. The ERTC is now available through June 30, 2021.

Advance Payment of ERTC. Beginning January 1, 2021, employers with less than 500 employees can apply to receive the credit in advance for up to 70% of average quarterly wages paid in 2019 (or 2020 for businesses not in existence in 2019). For seasonal employers, wages from a specific calendar quarter may be used instead of the average. The advance will be reconciled against the actual credit later on, increasing the employer’s payroll tax for the calendar quarter if there is an excess.

Extension of SBA Loan Debt Relief

Extension of Monthly Payments: The debt relief program provided for by the CARES Act, which covers principal, interest and fees payments for eligible SBA 7(a) Loans has been extended for an additional 3-month period, with payments starting on February 1, 2021. There is an extended 5-month period after the initial 3 months for businesses operating under certain hard-hit industries (food and entertainment, educational services etc.).

Maximum Covered Payments Per Month: The SBA will only cover a maximum of $9,000 for each month, with the excess amount to be reported as additional interest to be paid at the end of the loan period.

Limitations on Specified 7(a) Loans: Borrowers cannot receive debt relief assistance for more than one 7(a) loan that were taken out between March 27, 2020 to October 26, 2020.

Tax Implications: The debt relief is also excluded from income, with no expense disallowance as a result of the income exemption.

SBA Loan Enhancements

Temporary Fees Waiver. The SBA is expected to waive or reduce administrative fees related to SBA 7(a) and 504 loan applications.

Increased 7(a) Loan Guarantee. The SBA will now guarantee at least 90% of the balance of 7(a) loans, up from 75% to 85% (depending on loan amount).

SBA Express Loans. The maximum loan amount is temporarily increased to $1 million and the SBA guarantee rate is modified to the following:

- Loans less than or equal to $350,000 – up to 75%

- Loans greater than $350,000 – up to 50%

All of the above provisions are only applicable through September 30, 2021, as the act specifically provided for a prospective repeal by October 1, 2021.

Grants for Shuttered Venue Operators

Eligibility Requirements The person or entity must be a live venue operator or promoter, which includes the following:

- Theaters

- Museums

- Cinemas

- Talent managers and representatives

The grantee must have been operational on or before February 29, 2020 and must have experienced at least a 25% reduction in gross receipts on a quarter-to-quarter basis. The grantee must also be operational, or is expected to resume operations, by the grant date.

Exclusions. The Act specifically prohibits the following persons or entities from receiving the grant, that meets the following criteria:

- At least one of the following:

- Publicly-owned companies

- Receiving more than 10% of gross revenue from Federal funding

- At least two of the following:

- Operating in more than one country

- Operating in more than ten states

- Employing more than 500 employees as of February 29, 2020

Priority Periods The grant is provided on a priority basis with applicants who had experienced a 90% reduction in gross revenues on an April to December 2019 and 2020 comparative period, getting prioritized in the first 14 days. Second priority (over the next 14 days) is provided to applicants with a 70% reduction in revenues. Applications from the remaining eligible applicants will be processed after the initial 28-day priority period.

Grant Amount The maximum grant amount that an eligible person or entity can receive is the lesser of:

- Operational before January 1, 2019 – 45% of gross revenue for 2019;

- Operational during 2019 – average of full months revenue multiplied by 6; or

- $10 million

Supplemental Grants Additional grants may be awarded after the initial grant if the grantee still experiences a 70% reduction in gross revenues by April 1, 2021. The SBA however, must process all initial grant applications first before supplying any supplemental grants. The supplemental grant is limited to 50% of the original grant received.

Use Of Grant Funds The proceeds from the grant may be used for most of the operational and business expenses, except for the following:

- Purchase of Real Estate

- Payment of Interest for Debts Incurred after February 15, 2020

- Capital Investments

- Political Contributions

The funds are to be used within one year of disbursement (18 months for supplemental grants) and may be used for expenses incurred during the covered period March 1, 2020 to December 31, 2021 (March 1, 2020 to June 30, 2022 for supplemental grants).

Tax Implications: The grant received is excluded from income, and no deductions are disallowed as a result of this income exemption.

Meals Deduction

Temporary Allowance of Full Deduction for Business Meals. For amounts paid or incurred after December 31, 2020 and before January 1, 2023, expenses for food or beverages provided by a restaurant are eligible for 100% deduction.

As always, if you have questions about how this bill impacts you, please contact our office.